Buyers lamenting a shortage of inventory in the Toronto-area real estate market will have a rush of fresh listings to sort through this month.

But the added supply is coming into an unsettled market where agents say some retro practices are making a comeback and new tactics are emerging.

Sales in the Greater Toronto Area dropped 5.2 percent in August compared with the same month last year, according to the Toronto Regional Real Estate Board.

New listings, meanwhile, jumped 16.2 percent in August compared with August 2022 while the average price of $1,082,496 last month was nearly flat.

In an uncertain market, Rochelle DeClute, broker with DeClute Union Realty, is seeing an increasing number of home and condo owners decide to sell their existing property before they buy a new one. That’s a shift in the trend of recent years.

She adds that sales last month varied within different pockets of the GTA.

The Beaches neighbourhood, where Ms. DeClute does much of her business, saw a stronger August than last year. In that area, 38 properties changed hands last month compared with 26 sales in August 2022.

Ms. DeClute believes buyers were willing to make a move because competition for properties was less intense than in the spring. In many years, August is the month when buyers try to find a deal on a property that has been sitting on the market.

“There are typically fewer houses on the market but better deals,” she says.

The average price in the Beaches dipped to $1.4-million at the end of August from $ 1.5 million one year earlier, she says.

Increasingly, sellers are wrapping their minds around the current landscape, she says.

“We’re seeing the price change happen in a couple of weeks,” she says of the more pragmatic sellers.

In an added twist, sellers are sometimes chasing buyers these days.

“Strategically, if a buyer is interested, there’s no reason the seller can’t write an offer to the buyer,” Ms. DeClute says.

Her office launched such a bid recently just as interest rates were on the rise.

A house with an asking price around the $2.5-million mark was listed with a plan for the sellers to review offers on a scheduled date.

The first prospective buyers to look at the property quickly moved to pre-empt the bidding process with an offer of $2.68-million. The buyers made clear they would not return on the scheduled offer night if their “bully” offer wasn’t accepted.

The sellers wanted to give more people the opportunity to see the property so they turned down the offer.

On offer night, the bullies stayed away and no buyers came to the table.

The sellers then revived negotiations by writing an offer to the first bidders at$30,000 less than their original bid.

They accepted and both sides were very satisfied with the final price of $2.65-million, Ms. DeClute says.

Agents need to be creative and ensure that both sides feel they ended with a win, she adds.

Ms. DeClute says the current environment remains a sellers’ market but she is also seeing an increase in motivated sellers.

Many homeowners are shocked, for example, when the time comes to renew a mortgage and they see payments double. Some are deciding to step out of homeownership as a result.

In her experience in the east end, the number of days between signing an agreement and closing the deal has also lengthened, she says.

Ms. DeClute says buyers with an existing property want to ensure they have the time to sell it before the closing on a new one.

Legal text known as a “flexible closing clause” is making a return, she says, as buyers ask for the option to extend or advance the closing date by a specified amount of time.

Ms. DeClute has also seen cases where buyers do not have any flexibility written into their sales agreement but they ask to move up the closing date so that they can take advantage of a favourable interest rate for a pre-approved mortgage. Sellers sometimes refuse because they have made their own plans around the agreed-upon closing date.

The buyers may choose to accept the closing without vacant possession so that the funds are transferred while the sellers still live in the house. Lawyers often balk at the arrangement, Ms. DeClute says, but the compromise has saved many interest rate holds for buyers.

Cheri McCann, broker with McCann Realty Group, says some properties are moving quickly in the early days of the fall market but competition is less intense than it was earlier this year.

In the core, houses in neighbourhoods such as the Junction and Leslieville were still drawing multiple offers in the quieter summer months, Ms. McCann says, but she has noticed a drop-off in activity in areas north of Highway 401.

Above the $3-million level, sales are slower, she adds, but buyers with deep pockets are still booking showings.

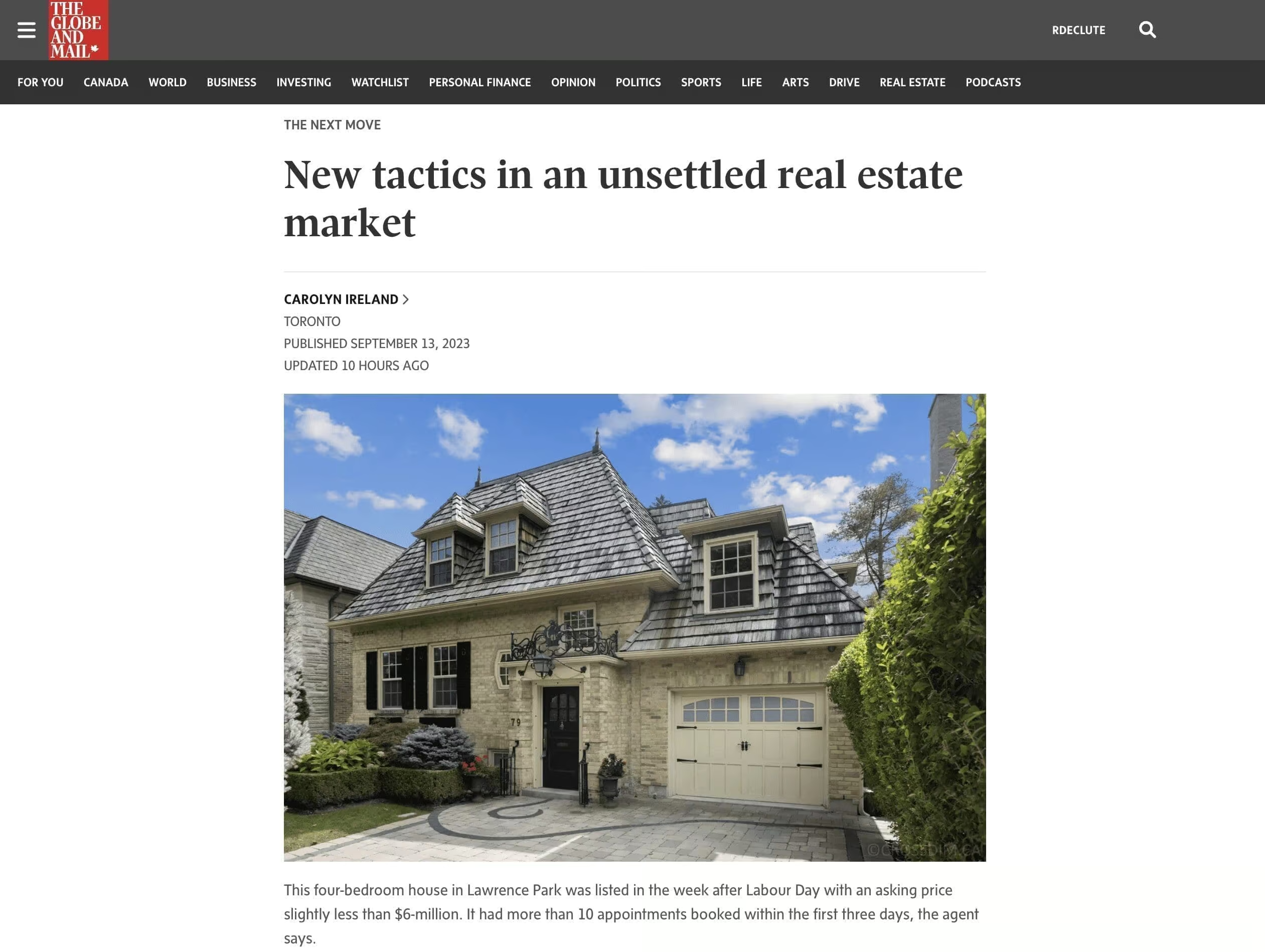

In the week after Labour Day, she listed a four-bedroom house in Lawrence Park with an asking price slightly less than $6-million. The house at 79 Dawlish Ave. had more than 10 appointments booked within the first three days, she says.

The combination of high interest rates, prices and taxes is weighing on many potential buyers, she says.

In midtown Toronto, properties that were changing hands for $2.1-million or $2.2-million are now more likely to fetch $1.9-million or $1.95-million.

Victor Tran, mortgage specialist with rates.ca., says 90 percent of the calls he received in July and August were from existing homeowners and investors who were looking for advice on renewing or renegotiating an existing mortgage.

Many first-time and move-up buyers appear to be waiting for rates to come down, he says.

“Purchase transactions have been down the drain.”

The Bank of Canada’s decision to hold its trend-setting interest rate steady in September came as a relief for many homeowners with a variable rate mortgage or a line of credit, he adds.

Most of the people he sees struggling are holding investment properties, Mr. Transays, adding that he has not yet had clients who are giving up a principal residence.

Mr. Tran predicts an uptick in inventory in the coming weeks as sellers enter the traditional fall market. But he adds that some owners are also buckling under financial pressure and feel they have no choice but to sell.

“A lot of people are on edge.”

Buying, Selling, or Have Questions?

We can help. Connect with our East End experts today!