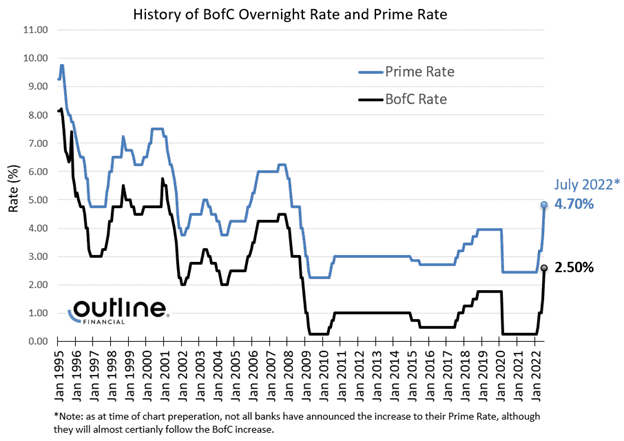

Why did the Bank of Canada (BofC) increase their overnight rate by 1%?

In its accompanying press release the BofC said: “With the economy clearly in excess demand, inflation high and broadening, and more businesses and consumers expecting high inflation to persist for longer, the Governing Council decided to front-load the path to higher interest rates by raising the policy rate by 100 basis points. The Governing Council continues to judge that interest rates will need to rise further, and the pace of increases will be guided by the Bank’s ongoing assessment of the economy and inflation.” Further clarification was provided in the BofC’s Monetary Policy Video and Report where they stated: “By front-loading interest rate increases now, the goal is to get inflation back to the 2% target with a soft landing for the economy. This will avoid the need for higher interest rates down the road.” While the Bank of Canada considers today’s change as a proactive move, they have also said they still expect further increases will be needed this year. The extent of these increases has yet to be clarified, and we will be watching closely whether the currently forecasted peaks for the overnight rate shifts upward in the coming weeks.What could this mean for you?

While DeClute Real Estate and the Outline Financial team is on standby to discuss how these changes may impact your specific circumstances, we have included a few scenarios below that cover our most frequently asked questions from existing mortgage holders as well as those looking to secure a mortgage.Scenario 1: I currently have a variable “non-adjustable” mortgage (VRM), how will this impact me?

- In this scenario your mortgage payment will remain the same, however, a higher proportion of each payment will go towards paying interest vs. principal. The net impact is an extended amortization (total amount of time to pay off your mortgage will be longer).

- What can you do? As the variable rate remains below fixed rates, you could keep everything the same and continue with the same monthly payment. Alternatively, you could increase your mortgage payment to ensure you remain on pace with your current amortization schedule.

- Be aware of your Trigger Rate. As interest rates rise, there may be a point where your set VRM payment can no longer cover the interest calculated (and charged) on the outstanding mortgage amount. This is known as the Trigger Rate. In this scenario your mortgage may have an increasing balance unless the payment is increased enough to cover the outstanding interest.

- For questions on your payment strategy, trigger rate, or to review potential pros/cons of converting your current VRM into a fixed mortgage, please reach out at any time.

Scenario 2: I currently have a variable “adjustable” mortgage (ARM), how will this impact me?

- In this scenario, your mortgage payment will automatically increase to ensure you keep pace with your current amortization schedule. If you would like to discuss future interest rate projections, or the potential pros/cons of converting your ARM into a fixed mortgage, please reach out at any time.

Scenario 3: I currently have a fixed-rate mortgage, does the recent change impact me?

- If you have a fixed-rate mortgage, there is no impact on your mortgage payment (or amortization) as you have received a guaranteed rate for the duration of your mortgage term. Only when your mortgage comes up for renewal, or if you sold and purchased a new home, would you potentially be impacted by higher rates.

Scenario 4: I am currently looking to secure a new mortgage, a pre-approval, or refinance an existing mortgage.

- Fixed or Variable? While each circumstance is unique, there are a couple of key points that you will want to keep in mind if trying to decide between the two.

- Variable rate mortgages are directly impacted by the Bank of Canada as described in Scenario 1 and 2 above and your interest costs will move up or down based on the BofC rate decisions making them more volatile. However, variable rate mortgages are generally more flexible than fixed rate mortgages in terms of penalties if you ever need to break your mortgage.

- 5-year fixed mortgage rates typically follow the Government of Canada 5-year Bond Yields which is the market’s view/prediction of where interest rates will be in the future. The 5-year bond yields actually started moving upward back in early 2021 in anticipation of the Bank of Canada rate increase(s) we are now seeing in 2022. Bond yields (and fixed rates) are currently at the highest levels since 2008, but have leveled off recently.

- 2, 3, and 4 year fixed mortgages. As many economists believe our rapidly growing economy could turn recessionary in the next few years (resulting in lower interest rates), many clients are opting for shorter term fixed rates given the benefit of lower rates vs. the 5-year fixed, a fixed payment vs. the ARM, and a guaranteed interest rate vs. the VRM.

- Mind the Gap – when deciding between fixed and variable it is important to analyze not only the difference in the current rates, but also the expectation of future Bank of Canada rate changes. For example, if the current fixed rate (a sure thing over the term of your mortgage) is 1.00% higher than the current variable rate option (subject to change over the term of your mortgage), will that initial 1.00% “GAP” or “initial rate savings” be sufficient to protect you from any future Bank of Canada rate increases? Every situation is unique and we have a number of tools that can help model out the expectations for your specific circumstances.

Important Reminder: Stress Test and Variable Rate Pre-Approvals

- Stress Test Reminder: To help ensure clients can absorb interest rate shocks, all banks and federally regulated lenders are required to qualify clients’ based on a “Stress Test” interest rate set at the greater of 5.25% or the clients’ actual mortgage rate +2.00%.

- Why does this matter? After the recent Bank of Canada increase, the stress test rate has increased for variable rate mortgages which will reduce a clients’ borrowing/purchasing power (rule of thumb: each 1% increase in the stress test rate is equivalent to an approx. 8% reduction in borrowing/purchasing power). If you have an existing variable rate pre-approval, or would like to secure a pre-approval, please contact a member of the Outline Financial team so we can help quantify the impact of this change.

For a customized analysis of which rate or product option might be right for you, please contact us so we can get you in touch with a member of the Outline Team.

For a customized analysis of which rate or product option might be right for you, please contact us so we can get you in touch with a member of the Outline Team.

Buying, Selling, or Have Questions?

We can help. Connect with our East End experts today!

Contact Us